Since I’m going to reach financial independence next year and will likely quit my job before the end of the tax year, I decided to figure out when would be the most financially optimal time to quit.

Due to various tax laws, there are certain income levels that are worthwhile to stay under and, surprisingly, there are income levels that it actually pays to stay above.

Since I only plan on working part of the year, I can determine the most optimal income level and then quit at the appropriate time to maximize my earnings.

Earned Income Tax Credit

One of the reasons to have more rather than less income is to qualify for the full Earned Income Tax Credit (EITC). The EITC is a refundable tax credit that phases in, levels off at a certain income level, and then decreases until the income limit is exceeded (see income limits here).

The beauty of a refundable tax credit is that even if you don’t pay any federal income taxes, you can still get the credit. For families that have 3+ children, the tax credit could exceed $6,000 so it’s definitely worth paying attention to.

Dividend Tax Rate

The next income limit to consider, and the most important in my opinion, is the upper bound of the 15% tax bracket. If you stay within or under the 15% tax bracket, you can enjoy tax-free qualified dividends and long-term capital gains. For people who live off of their investment portfolios, this is a big deal.

Semiretirement to Early Retirement

All this research into ideal income levels got me thinking about semiretirement. Many people, myself included, imagine doing some sort of part-time work after financial independence. Why not include that part-time work into your plans and quit your full-time job earlier?

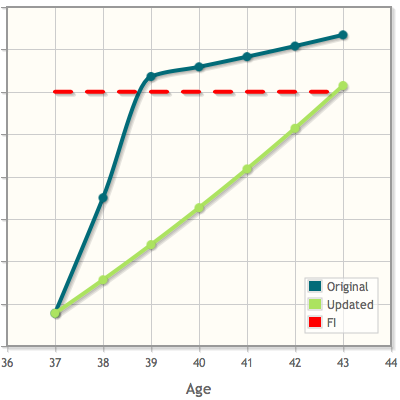

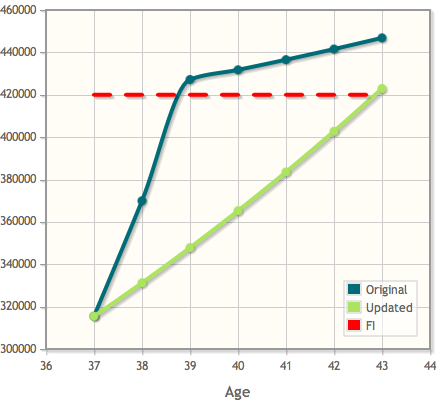

As we saw in the Retire Even Earlier post, the Lab Rat’s working career is already down to just 9 short years. What if by the 7th year he’s had enough and decides to quit his full-time job? Since he’s quitting two years before FI, he’s going to have to continue working part time so let’s explore a few of his options.

Cover Expenses

Imagine the Lab Rat is an avid skier and plans on spending his early retirement skiing some of the best mountains in the world. After moving to a mountain resort, he decides to get a part-time job on the mountain, in order to meet new people and get a free employee season lift pass. Since he wants to spend the majority of his time skiing, he only works enough to cover his expenses of $16,800 per year.

To maximize the value of his income, he decides to use retirement account contributions to reduce his earned income to the $7,000 – $8,000 level, which will allow him to qualifying for the full Earned Income Tax Credit.

Here is what his part-time situation would look like:

Wages: $17,700

401(k) contribution: $10,000

FICA tax: $1,354 ($17,700 * 7.65%)

EITC: $487

Federal Income Tax: $0

Since he’d but putting $10,000 of his earnings into retirement accounts, he’d have to withdraw an equal amount from his taxable investments to cover his annual expenses. Luckily, his long-term capital gains and qualified dividends (which he’ll need to keep under $3,200 to qualify for the EITC) will be taxed at 0%.

Here is what his path to FI would look like in this scenario:

Not only does this plan allow the Lab Rat to start his perfect life two years earlier, he can ease his way into early retirement and can still reach full financial independence before his 43rd birthday.

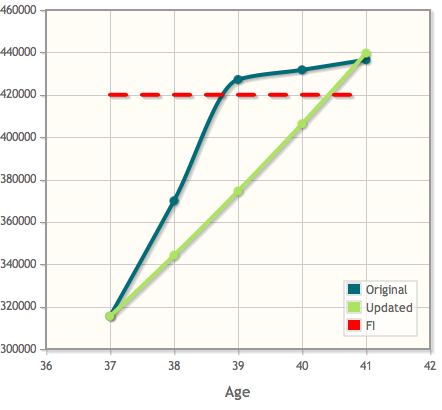

Half Time

Imagine instead the Lab Rat wants to quit his job and travel around the States for a few years. When he hands in his resignation, however, his boss asks if he’d be willing to stay on as a remote consultant. The Lab Rat agrees but only commits to working 20 hours a week.

Staying on at 50% allows him to still qualify for all the benefits that full-time employees enjoy but he has much more time to do interesting and exciting things.

Again, to maximize the value of his income, he decides to use retirement account contributions to reduce his earned income and adjusted gross income to within EITC income limits.

Here is what his half-time situation would look like:

Wages: $30,000

401(k) contribution: $17,500

Employer 401(k) 5% match: $1,500

HSA contribution: $3,250

IRA contribution: $1,500

FICA tax: $2,046 (($30,000 – $3,250) * 7.65%)

EITC: $400

Federal Income Tax: $0

Again, he’d have to withdraw from his taxable investments to cover his annual expenses but the long-term capital gains and qualified dividends would be taxed at 0%.

Here is what his path to FI would look like in this scenario:

This plan looks even better because he can quit full-time work two years earlier than the original scenario and still reach full financial independence before his 41st birthday.

Emotional Challenges of Early Retirement

Early retirement is a very drastic change so going from working full time to not working at all could be a big shock to the system. Working part time for a few years could be a nice transition into early retirement and could allow you to leave full-time employment years earlier.

I know personally I’m struggling to come to grips with the idea that I’ll actually be quitting my job next year. I’ve spent so many years planning for FI and building up my savings that I think it will be difficult to actually walk away from work completely and start drawing down from my accounts. Semiretirement could be a great way to smooth the transition into early retirement and could help minimize the emotional challenges associated with financial independence.

Great post and somewhat timely for me. I’m considering a flavor of semi-retirement as well. I like that you acknowledge there is an emotional element to ER (or semi-ER) as well. While I haven’t yet perused your entire site, is there room in the lab for more research around the psychological aspects of retirement?

There is always room in the lab for additional research! I’m actually starting my preliminary research for my master’s thesis so I’ll likely be investigating some of these types of topics in greater detail soon.

What is your flavor of semiretirement like? Are you heading to Spain a bit earlier than planned?

Yes, we’ll probably go as early as next year. Call it a mini-retirement of sorts.

I love the point you make about FI being drastic for some. I am one of those, for sure. Although I am extremely motivated to reach FI in the next 10 years, I will be doing so by “weaning” off of work. It’s also healthier than working myself to a pulp to save more ferociously. We’ll see how it works out…your posts may change my mind, though!

As I get closer to the goal, it’s becoming clearer and clearer how drastic of a change it will actually be.

I took a look at your site and noticed you just spent some time in Vermont. I’m actually a Vermont resident so I’m curious where you stayed when you were up here?

Weston! Home of the Vermont Country Store, Playhouse, and my camp. I’m driving up today.

I’ve never actually been down that way before. Sounds nice though so my wife and I will have to go check it out sometime.

Drive safe and enjoy your visit!

You are welcome any time. The concerts are free in the summer…perfect for a Mad Fientist and his wife. http://www.kinhaven.org

Look at this, one of my new favorite blogs, and all these locals… I’m in Chester, VT- very close to Weston. We have a few rentals in the area, climbing our way to FI slowly and enjoying the process. Loving your work Mad Fientist, thanks for sharing!

Thank you for this post! This is timely for me as I’ve recently come to see my part time work as being semi-retired. My path has been a bit different with the primary reason I do not work full time being my two kids. I have worked part time since the first one was born. I will reach FI only a few years later working part time and spending lots of time with them as I would have had I worked full time and hired others to care for them. Easy trade off for me to make. I admit it was not fully intentional at the time I made the decision to stay home part time. I have recently started following you and Mr. Money Mustache and have learned so much!

Thanks for the comment, Sara!

If more parents ran the numbers, I bet more would make the same decision you did. I was shocked when one of my friends told me how much he pays for daycare! When you combine those kinds of childcare costs with the higher income taxes, additional commuting costs, etc. that are associated with full-time employment (not to mention the time away from your kids), part-time work starts to look very appealing!

Really nice job with this post! Been following your posts for a while and just wanted to comment on how well you broke this down. I’ll be considering this type of strategy down the road and to see the tax implications explained so simply is helpful. Well done.

I really appreciate you taking the time to write, Dan. I often worry that my posts have too many numbers or, on the opposite end of the spectrum, lack enough detail and explanation so I’m happy to hear I struck a good balance with this post at least.

“I know personally I’m struggling to come to grips with the idea that I’ll actually be quitting my job next year. I’ve spent so many years planning for FI and building up my savings that I think it will be difficult to actually walk away from work completely and start drawing down from my accounts.”

If you can, I would be quite grateful if you start documenting your feelings and how they develop over the next two years or so. I know it’s a lot to ask to keep constant track of such things, but if you’re up for publishing even a small part it would be of immense use to people like me who are looking at an impending end date less than 5 years out …

That’s a great idea, Greg. I definitely think the emotional challenges are a very important, but not often discussed, aspect of early retirement so I’ll do my best documenting what I go through. Thanks for the suggestion.

I am from VT too. I dont find vermont to be a good place to live in term of going FI.

Yeah, it’s not the best but it’s definitely not the worst either. While I do love it here, I’m looking forward to heading off to more FI-friendly places next year.

Didn’t u set up lending club? How did u do that from vermont?

Hi Alan, I think you may have me confused with someone else (maybe MMM). I haven’t set up an account with Lending Club and it looks like I currently wouldn’t be able to, since I’m a resident of Vermont.

Thnaks. Can’t do vanilla reloads, blue bird, Amex prepaid, lending club…

That is why I say VT is. OT very good to FI.

Luckily I work in New Hampshire so I was able to get an Amex Bluebird delivered to my office. Since I live so close to the border, I can also pick up Vanilla Reloads when I need them :)

Can you explain the advantage of using per paid cards? Especially versus mileage credit cards? Might be a good post.

Hi Karen, I use prepaids/Bluebird/etc. in conjunction with mile-earning credit cards. For example, sometimes Staples has deals on prepaid cards (e.g. free $15 Staples gift card when purchasing a $200 Visa prepaid) and when they do, I use my Ink Bold to purchase the $200 gift card (which gives me 5 Ultimate Rewards points per dollar at office supply stores), I load the gift card onto my Bluebird card, then I use the Bluebird bill pay feature to pay some bills that I wouldn’t normally be able to pay with a credit card.

Do you have any advice on how to keep track of what card to use where? Some you get extra points at office supply stores, restaurants, gas stations, etc. but I wish there was a website I could just plug in the cards I have and it would tell me which one to use where!

Hey Dustyn, I was actually just updating an Evernote I have that contains a list of what cards to use for what purchases (I just applied for a new card today). I’ve heard of people writing on the cards themselves so that may be a good option if you don’t have Evernote on your phone.

Do u pay VT state income tax?

Yes, even though my employer is in NH, they know I live in VT so VT state income tax is withheld from my paycheck.

Mad Fientist, I hope you’re doing well. First off, great article and thanks for sharing! Just a few clarifications from a financial planning perspective…

The Earned Income Tax Credit would not apply in either of the examples above. This gets a little tricky, but basically the LTCG and the Qualified Dividends (even at 0% tax rate) increase your AGI. Even though they do not increase your federal tax owed, they do push up your AGI and therefore phase you out of this tax credits.

Another note is the LTCG and Qualified Dividends also could push you out of the 15% tax bracket as well (as it increases AGI and Taxable Income, even though it doesn’t add to your tax owed!). In your examples above, this did not occur as the person stayed below the 15% tax bracket ($36,250) even with the LTCG and Qualified Dividends.

Lastly, I would also consider the Retirement Saver’s Credit. This credit allows a person to offset up to $1,000 (or $2,000 MFJ) in tax owed. This credit is not refundable, but could still help if used properly.

Thanks again and keep up the great work!

Nick, good to hear from you again!

I agree that long-term capital gains and qualified dividends increase the Lab Rat’s AGI in these scenarios but it doesn’t increase it enough to exceed the EITC income limits.

Based on the numbers I used, only ~15% of the money withdrawn from the taxable accounts would be long-term capital gains or qualified dividends. Therefore, from my calculations, the AGI in both scenarios would be around $9K, which is well within the EITC income limits. Let me know if I’m missing something here.

Thanks a lot for the heads-up on the Retirement Saver’s Credit! I’m going to read more about it tonight and will be sure to update the post if the Lab Rat is able to take advantage of it in these scenarios.

Thanks for the clarification, Mad Fientist! It makes perfect sense now based on your assumptions. Most of the employees I deal with usually have a lower cost basis :) I just crunched all of the numbers and we are at a very similar spot now.

This strategy would work well if you used specific ID for your taxable account cost basis to maximize your flexibility. In your examples, the Retirement Saver’s Credit would not help because there is no federal tax to offset. Still nice to have in your back pocket when you do owe tax…might not be the case for us :)

Haha yeah, I can’t imagine you get many clients with those types of numbers.

The Retirement Saver’s Credit is definitely one to keep an eye on (even though the Lab Rat doesn’t have any tax to use it on) so thanks a lot for mentioning it.

Although it adds a bit of pressure when writing these articles, it’s great to know other people out there are checking my numbers and making sure everything I write is accurate. I spend a lot of time reading over documentation and checking my calculations but it’s good to have someone else scrutinizing everything so I really appreciate you taking the time to run the numbers yourself!

Anytime, keep up the great work. Love the site!

Good article with a lot of information that’s pertinent for me! I’ve just started to think about what the ideal time of year to retire would be, though I suspect the tax implications are going to be drowned out by other factors for me (bonus timing, how much I enjoy where I currently live during different times of year, attempting to limit impact on employer to not burn any bridges, etc.)

The “cover expenses” option you’ve listed is basically exactly what I’m planning on doing, though I’m not expecting to work steadily as you describe — just planning to earn in total about what I spend in total over the first 5-10 years of “retirement.”

It’s great when you work out the details for me on the half-formed plans in my head.

Hey Roger, good to hear from you again! I suspect other factors will play a part in when I actually quit as well but I’ll definitely be keeping the things I wrote about in mind when I make my decision.

Glad to hear this article was right up your alley!

I started my five-year experiment with semi-retirement a year and a half ago. It turns out that with consulting, I work about half the time and make about just as much money as I used to. In the meantime, I have extra time that I can use to explore other interests or business ideas, and that works out nicely. My expenses have been right in line with my predictions. I think I might even have enough assets to be mostly retired.

I’d definitely recommend “phasing in” retirement like that, especially if your skills are good for consulting or short-term projects. My background is in web development and enterprise consulting, and I found my first clients because I was blogging about my plans for semi-retirement. =) Every so often, I take extended time off (for example, all of last August) so that I can get deeper into experimenting with Proper Retirement. I like it, so I’m working on arranging my life to do more of that.

Phasing into retirement also lets you test the idea with less commitment. You can still maintain your social and professional links and you don’t have to worry about completely rejigging your identity, but you have the space to explore more.

That’s great to hear semiretirement has worked out so well for you. Consulting seems like a great transition into early retirement and is something that I may explore. I can imagine being offered a telecommuting arrangement when I eventually leave my current job so depending on how good the offer is, I may do some part-time consulting for a bit as well.

This was a really helpful post as I’m working on my escape plan, which will hopefully take place in the next three years. As a result, I’ve been trying to gather as much information as I can about minimizing taxes, harvesting capital gains, ROTH conversions, etc. while balancing that with the likelihood that I’d either work part-time or manage my rental property.

In looking at the IRS site on EITC, however, I noticed a little note that said, “investment income must be $3,300 or less for the year.” Does that mean then that I won’t be able to draw down investment earnings beyond $3,300? How would that work as an early retiree?

Hi Joyce, glad it was helpful.

You are correct that if you have over $3,300 of investment income (e.g. rental income, dividends, capital gains, etc.), you won’t be able to claim the EITC.

If you don’t have much dividend/rental income, however, and instead fund your early retirement by selling off assets in your portfolio, you still may be able to qualify for the credit.

For example, imagine the Lab Rat bought 1000 shares of stock x for $15 per share and then to fund the first year of his early retirement, he decided to sell those 1000 shares for the current price of $16.80 per share. The sale of those shares would provide the $16,800 of income that he needs for the year but his investment income would actually only be $1,800 (($16.80 – $15) * 1000 = $1,800 worth of capital gains).

So while it’s possible to do, it will likely be much harder to qualify for the EITC once you start relying on your investments after early retirement.

Great stuff!

I’ve been devouring your blog (as well as MMM) for about a month and half now. I’m so glad I found this stuff early!

So, am I correct in thinking that taxable accounts are what funds early retirees to retirement age, and then tax-advantaged accounts for after retirement age?

Glad to hear you’re enjoying the site, Tyler!

You are correct in your thinking but it should be noted that you can also use tax-advantaged accounts prior to standard retirement age (check out this post and this post).

Hope this comment is not too late to be useful, but just want to point out that another important income level threshold to be mindful of is the one that determines eligibility for subsidies under the Affordable Care Act. You don’t want your income to be too low to qualify for subsidies (unless you want Medicaid as your health insurance and you live in a state where the “Medicaid gap” is not an issue), but the subsidies also start to phase out as your income gets higher. Since these subsidies can be worth many thousands of dollars per year, I would rank this as one of the higher priority opportunities for income optimization.

And, Mad Fientist, I would like to add to the chorus of voices thanking you for this truly excellent blog!

You’re definitely not too late to be useful, brooklynguy! That’s an excellent point and ACA is something everyone needs to keep in mind when determining how much income to have during semiretirement.

In fact, it’s so important that I’ve made a note to either update this post or create a brand new one all about it so thanks very much for the comment!

Saw this one linked in the comments from another post. Do you have any thoughts about Sagmeister’s idea of taking a year off periodically? (link: http://blog.ted.com/2009/10/02/the_power_of_ti/). Seems like a good idea for those of us on a longer timeframe for retirement, but you’d lose access to lots of tax advantaged accounts, I would think…

I actually did a little bit of that before I got on the path to FI. I would use some of my savings to take big chunks of time off (since my wife and I moved between the US and Scotland a few times, we used that as an excuse to take some time off during those transition periods).

If I were to do something like that now, I’d arrange it so that I’d take off in June and return the following June. That way, I could earn the optimal amount of income for each year (as mentioned in this post) and still be able to max out my retirement accounts.

I think it’s a great idea and I bet if you took the time to plan it, you likely wouldn’t lose out on too much income since you’d be saving so much in taxes.

Thanks! The June-June schedule is a really good idea.

17,700; minus 10,000 for 401k; minus 1,354; plus 487; plus 3,200; equals 10,330. How do you cover expenses of 16,800 with 10,330?

Not sure what I missed.

Hey Kurt, he’d have to withdraw $10,000 from his taxable account to cover his expenses but if he keeps his long-term capital gains under $3,200, he’d still be able to get the EITC. For example, if he bought 80 shares of stock x for $100 each and then when he decided to sell to fund his expenses, the share price rose to $125 ($125 * 80 shares = $10,000), he’d still be able to fund his expenses while keeping his long-term capital gains under $3,200 (in this scenario, the gains would only be $25 * 80 = $2,000). Make sense?

Another excellent article! Although I’m still new to all of this new way of thinking(taking the red pill only 1 month ago lol) and on the ground floor the scenario’s and #’s make things easy to digest. And your info is in the league and in conjuntion w/ MMM, Jim and Jacob ;) The 4(maybe I’ll find others) different styles and info together make the goal of FI seem fun and attainable. It’s been an eye opening process. I grew up with no financial guidance(neither did my wife) and I wish I would have found these sooner. But at 37 it’s still not too late and I’m determined with the help of you guys that have these great blogs to do an M180 and hopefully have an inspiring story to share.

Thanks, Mad NeoFite (great name, by the way)!

MMM, JLCollinsNH, and ERE are my three favorite blogs so that’s a huge compliment putting me in the same category as them.

Thirty-seven is definitely not too late to get started so I look forward to hearing more about your progress now that you’ve taken that all-important red pill :)

I think I am missing something here.

This sounds great for tax purposes and maneuvering yourself into taking advantage of the tax rules as they currently stand but say in the second example the guinea pig earns $30,000 but only keeps $6,104! Did I miss somewhere how the guinea pig is expected to live off of only 6k a year?

I get that he has other investments but those would be considered income if he begins to withdraw them correct? Maybe I am missing some other ‘trick’ you can use to not have other investments count as income.

It’s no longer early for me as I will be 62 in a few months. However, some of the ideas may still apply.

The last response to your posting is April 26, 2016. The folks in Washington DC have recently redone the tax laws. Has this changed the ideas given herein or were these changes cosmetic in regards to the ideas you espouse?

Man,……The more I read from sites like yours and Mr Money Mustache’s, the more I wish I had considered this 30 to 35 years ago.

One more question – It seems like a lot of people who want / take early retirement are software engineers. Why is this?