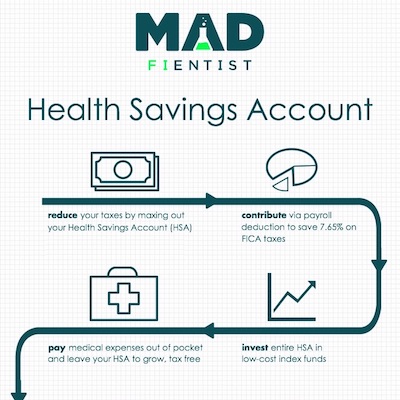

Latest ArticleThe Problem with the 4% Rule (and Why You Could Retire Even Sooner)The 4% rule wasn't made for early retirement. Here's a new withdrawal strategy that could allow you to retire even sooner!More Articles →Latest PodcastThe Best Advice from JL CollinsI collected all of the best advice from my three interviews with the author of The Simple Path to Wealth, JL Collins!More Episodes → Laboratory Instruments FI Spreadsheet Portfolio Manager FI Tracker Research Topics Tax AvoidanceInvestingTravel Hacking Popular ArticleHSA – The Ultimate Retirement AccountA Health Savings Account (HSA) is the ultimate retirement account because it can provide completely tax-free savings for early retirement!All Articles →Popular PodcastMr. Money Mustache – Early Retirement Made EasyMr. Money Mustache shares his financial independence and early retirement secrets in an interview for the Financial Independence Podcast!All Episodes →